FEBRUARY 14TH, 2026

Air Canada Q4 2025 Earnings Summary

Record Q4 Performance:

Air Canada delivered exceptional Q4 results with revenue of $5.8 billion (up 7% YoY), record Q4 adjusted EBITDA of $867 million (up 25% YoY, 15% margin), and industry-leading passenger unit revenue performance driven by strong premium demand. CEO Michael Rousseau emphasized structural advantages built over several years enabling mitigation of transborder softness through network/revenue diversity.

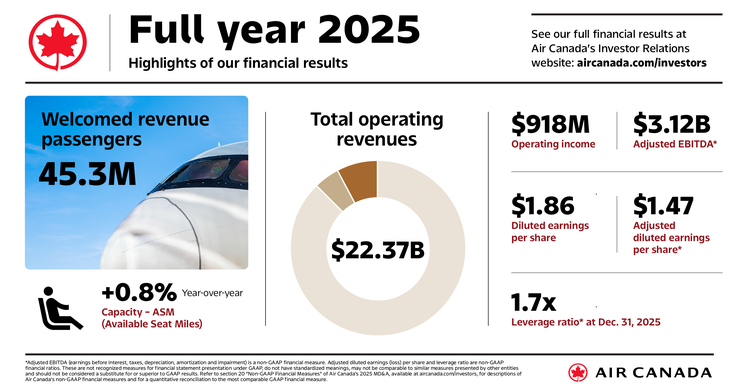

Full-Year 2025 Results:

Total revenue: $22.4 billion (up 1% YoY). Adjusted EBITDA: $3.1 billion (14% margin), exceeding guidance due to very strong demand in final 2 months. Free cash flow: $747 million (3% of revenue, targeting sustainable 5% long-term). Operating cash flow: $3.7 billion (>100% conversion from adjusted EBITDA). Returned >$850 million to shareholders via buybacks (funded entirely by free cash flow). CapEx deployment: $2.9 billion; took delivery of 14 aircraft.

Cost Performance:

Full-year adjusted CASK: $0.147 (up 6.7% YoY, upper end of guidance). CASK drivers: ~270 bps labor, ~140 bps depreciation (fleet investments), ~150 bps nonrecurring August labor disruption impact. Executed $150 million recurring cost reduction programs (management restructuring, process improvements, operational efficiency, spend management). Confident in multiyear structural improvements beyond 2026 from network expansion and modern fleet efficiencies.

Balance Sheet & Capital Allocation:

Liquidity: $7.5 billion (including undrawn revolver). Net leverage: 1.7x (below 2x target). Retired convertible bond, extinguishing ~$400M debt, avoiding issuance of ~18M shares. Early 2026: Repriced/upsized Term Loan B by $200M. Since 2024: Generated >$2B cumulative free cash flow; repurchased/retired >64M shares, returning >$1.3B to investors. Active NCIB targeting $2B buybacks and <300M fully diluted shares by 2028 (ended 2025 at ~307M shares).

Fleet & Orders:

A350-1000 Order: 8 firm aircraft (deliveries 2030-2032) + 8 purchase rights. Replaces oldest 8 A330s. Range capability enables new markets (Indian subcontinent, Southeast Asia, Australia) and improved economics on existing routes. Superior passenger/cargo payload. Fits within sustaining net CapEx target of ≤12% of revenue.

2026 Fleet Plan: Receiving up to 35 aircraft (majority second half): first A321XLR and Boeing 787-10 deliveries. A321XLRs unlocking new destinations (Berlin) and enhancing existing markets (Toulouse, Manchester); unveiling consistent year-round XLR product on North American routes for premium positioning. 787-10s deploying from Toronto initially. Rouge fleet transitioning to Boeing 737 MAX by end-2026 (subject to approvals), enhancing leisure competitiveness.

Sale-Leaseback Program: Signed nonbinding letters of intent for up to $2B in sale-leasebacks over next 24 months ($1B in 2026, $1B in 2027). Targets fleet ownership of 65-70% (down from >80%), bringing flexibility, capital efficiency, enhanced liquidity within net leverage targets. Capital cost competitive (typically within 100 bps of other financing).

Network & Revenue Strategy:

Geographic Diversification: International performance contributed ~90% of Q4 revenue uplift. Atlantic and Latin America posted load factor expansion; combined 4% YoY traffic growth. Successfully pivoted capacity during 2025 to Canada/Atlantic (summer) to fully mitigate reduced Canada-U.S. demand.

Sixth Freedom Growth: Record levels, revenues up 10% from 2024. Toronto/Montreal hubs connecting Europe-Latin America on counter-seasonal flows; Q4 results significantly above expectations. Summer 2026: Toronto 2nd largest transoceanic hub in North America (by seats), Montreal 5th largest transatlantic hub, Vancouver 2nd largest transpacific hub.

Premium Performance: 2025 revenues up 2% YoY (outpacing economy by 3 points), representing ~30% of total passenger revenues. Corporate revenue accelerated in Q4, up 8% YoY. Restored A220 schedules, achieved corporate growth in long-haul, staying competitive for business travelers. North Atlantic corporate traffic up ~30%.

Other Revenue Streams: 2025 other revenues up 15%; cargo revenues up 4%. Air Canada Cargo surpassed $1B revenue for first time since 2022, key player supporting long-haul flying. Aeroplan: Record >10M active members (up from ~4M at acquisition from Aimia); gross billings up 7%, card spend up 8%; third-party gross billings growth 7% in Q4. Revenue-based accrual program performing well; members qualifying for status increasing YoY.

Network Additions: 2025: Added 13 new destinations across 4 continents. Spring 2026: Starting transborder flying from Billy Bishop Airport (downtown Toronto) to major North American business centers. Summer 2026: Adding 7 destinations, reintroducing nonstop Toronto-China flights, extending year-round Toronto-Bangkok (only nonstop from North America). December 2026: Adding Sapporo and Quito.

2026 Guidance:

Capacity: 3.5-5.5% ASM growth (modestly constrained despite 35 aircraft deliveries due to back-half loading, Rouge fleet transition, planned retirements, mix of higher narrow-body/lower stage length ASMs).

Adjusted EBITDA: $3.35-3.75 billion (14-15.5% margin).

Adjusted CASK: $0.1505-0.1535 (reflects completion of major 10-year labor agreement renewals with remaining unionized workforce; $150M new cost reduction initiatives in strategic procurement/workforce productivity; ~$200M annual depreciation headwind continuing through 2027-2028).

Free Cash Flow: $400-800 million (reflects close to 100% adjusted EBITDA-to-cash conversion; net CapEx inclusive of $1B expected sale-leasebacks).

Fuel Assumption: CAD $0.90/liter; FX assumption CAD 1.36/USD (aligned with current market). ~17% of H1 2026 fuel hedged at CAD 0.69/liter (before taxes/fees). ~50% fuel procured from New York Harbor; remainder diversified (Asia, strong infrastructure East/West Coast).

Q1 2026 Outlook: Expecting adjusted EBITDA growth in absolute dollars and margin percentage, supported by unit revenue expansion + capacity growth. Inclusive of estimated impact from January weather disruptions and Cuba fuel shortage.

Operational & Customer Recognition:

Won 2025 Skytrax Best Airline in North America + 8 additional categories (more than any Canadian carrier). Only North American airline in Skytrax global top 20. Improved on-time performance and Net Promoter Score through schedule dependability and premium brand positioning. Successfully managed record Toronto snowfall/extreme cold demonstrating team strength and customer trust.

Market Dynamics:

Transborder: Relatively steady trends over past year with softness persisting. 2026 guidance assumes status quo (not worse, not better). However, favorable demand-capacity balance due to recent competitive moves supports constructive revenue rebound potential.

Domestic Canada: ~5% domestic capacity growth industry-wide, but demand-capacity balance favorable in Air Canada’s 3 hubs (Toronto, Montreal, Vancouver) per stated strategy. Some pressure in other Canadian cities with less exposure.

International Trends: Q1/Q2 2026: Seeing constructive environment with gains in load factor and yield, mostly in international markets (particularly Atlantic). Pacific: Load factor growth with stable yields expected through H1. Corporate/cargo tailwinds from Canada’s trade diversification strategy (30% increase in corporate traffic to Europe).

Flexibility: Suspended Cuba service following government advisories; reallocated capacity to other submarkets with minimal financial impact. Demonstrated agility to pivot capacity to areas of strength throughout 2025.

Cost Outlook Beyond 2026:

Labor reset concludes early 2027; expecting cost structure to grow meaningfully below inflation for next several years as scale increases. Fuel benefits expected (outside CASM) providing margin expansion. Depreciation headwind (~$200M annually) continues through 2027-2028 as CapEx cycle converges with depreciation over time (noncash item).

Strategic Positioning:

“Employer of choice for aerospace in Canada”; contributing meaningfully to Canadian economy. Building for long term with confidence that 2026 investments set stage for improved performance/efficiencies in 2027+. Targeting profitable growth, margin expansion, cash generation for sustained stakeholder value. 2026 characterized as “transitional year” absorbing cost pressures while receiving majority of fleet deliveries (H2 loaded).

Special Events:

World Cup 2026 (June): Net neutral impact; some European bookings for Canada games but overall neither positive nor negative for network.